by Rob Boon

If you are an employer, who pays staff a car allowance that is more than the .66 cents per kilometre, from 1st July 2015 you must withhold tax from these payments. While this legislation did not pass into law until September 2015, it is retrospective from 1st July 2015.

There are a couple of interesting points with car allowance payments, including the tax and other issues attached each.

1. The first is the ATO nominated maximum allowance.

2. The second is the modern award nominated car allowance

If payment of car allowance does not exceed the ATO nominated maximum of .66 cents per kilometre, then the payment to the employee is tax exempt. If however payment exceeds this .66 cent limit, then tax applies to the entire payment.

Under modern awards, and I refer here to the (Clerks – Private Sector Award) the car allowance to be paid is .78 cents per kilometre and would need to be taxed rather than be a tax-free payment.

As an example let’s consider an employee paid for 100 km at .66 cents and compare it to the same employee being paid at .78 cents. Let’s further assume that the employee has an annual salary of $52,000 p/a claiming the tax-free threshold under 2016 tax scale.

The employee being paid at the ATO rate of .66 cents would receive $66 tax-free. The employee being paid .78 cents would receive $78 less the additional tax payable on this payment; $27 leaving an after-tax payment of only $51 making the employee $15 worse off overall. Very interesting overall I am sure you will agree.

Here is the thing I find the most interesting and a little disturbing when speaking to FWA in relation to this. When I asked if I could pay the employee at .66 cents rather than the award which would leave the employee worse off, I was told that provided an employee was not left worse off, which clearly they are not, it would be acceptable. I then posed another question assuming an employer took this path trying to do the best for their employee. If the employer paid the employee’s car allowance at .66 cents leaving the employee better of; what position would fair work take should the employee at some point lodge a complaint that their car allowance was paid at the ATO maximum rate rather than the award rate? The response I received was that they would take the award rate and apply that. Surely this means that the ATO maximum per kilometre rates cannot be used when paying car allowance.

What this says clearly is that the best interests of the employee are not always the ultimate goal.

UPDATE:

The current situation now allows for car allowance to be processed through wages in two components.

- The current ATO Tax exempt value per Km of .66 cents. (2017-18 year which is reviewed each year.)

- Payment of values greater than the ATO tax-exempt Km rate.

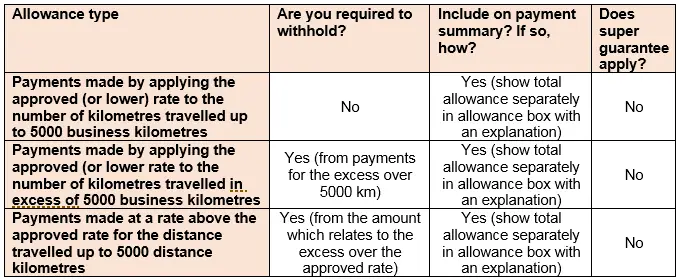

Table 2 – Cents per kilometre car expense payments using approved rate (ATO)